How Charitable Dollars Actually Reach Charities

Canada's payment infrastructure moves $411B daily. Charitable disbursements still rely on void cheques and manual batch files.

Jeff Golby

CEO & Co-Founder, WellFunded

Key Takeaways

- Canada's national payment systems clear over $411 billion every business day — but charitable grants still move on paper and manual processes

- Most DAFs and foundations rely on void cheques, emailed PDFs, and manually created batch files to disburse grants

- The gap between how consumer payments work and how charitable dollars move creates real risk for the sector

Most Canadians have probably never thought about how large charitable gifts move from an institution — a Donor Advised Fund, a foundation, or a corporation — to a charity. They probably assume it works like payroll, or bill payments, or any other routine bank transfer. Money approved, money sent, money received.

This isn't the case. The infrastructure that actually moves charitable dollars from funders to charities is far more fragile — and far more manual — than most people in the sector realize.

The rails underneath Canadian payments

Canada's payment infrastructure is massive. Payments Canada, the organization responsible for the country's clearing and settlement systems, processed over $103 trillion in 2025 — more than $411 billion every single business day.

That infrastructure is also modernizing fast. The Canadian Payments Act was recently amended to expand who can access national payment systems for the first time, opening the door to payment service providers, credit union locals, and clearing houses. The Real-Time Rail — Canada's first national instant payment system — is in testing now, with launch expected across 2026 and 2027. It will allow Canadians to send and receive irrevocable, data-rich payments in real time, 24/7, 365 days a year.

Behind all of this sits a small number of technology partners that are pre-cleared to interface directly with the banking system on behalf of businesses and organizations. These aren't household names, but they're the connective tissue between the apps you use and the banks that hold the money. When you link a bank account through a fintech product, one of these partners is doing the verification underneath.

The consumer and business payment world is heading toward instant, verified, always-on infrastructure. That's the direction.

How charitable money actually moves

Now consider what happens when a generous foundation, Donor Advised Fund, or corporation — we'll call them a Major Giver from here on — wants to send a grant to a Canadian charity.

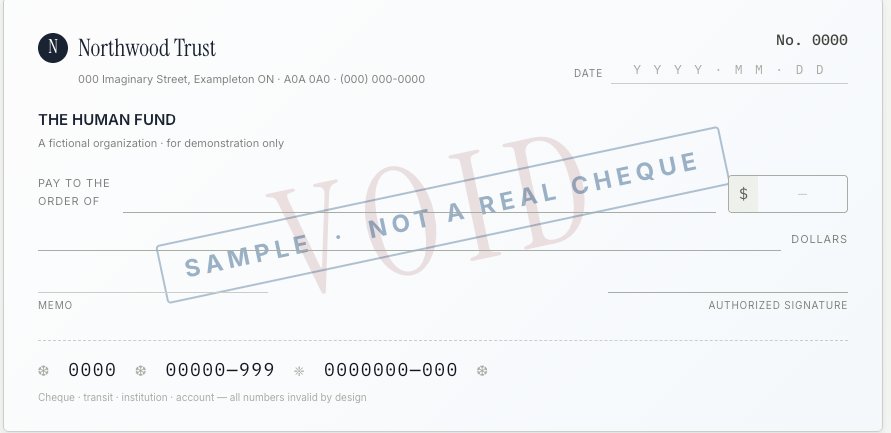

Someone — usually an administrator or finance team member — has to turn that approval into an actual bank-to-bank transfer. That means they need the charity's institution number, transit number, and account number. Where does that data come from? In most cases, a void cheque. Often sent by email. Sometimes by fax.

The administrator takes that data, enters it into a payment file — often a CSV or a standardized banking format — and uploads it to their financial institution for batch processing. If the Major Giver processes hundreds of grants per cycle, that's hundreds of line items manually compiled, reviewed, and submitted.

The challenge with this process is twofold. First, every manual touchpoint introduces the risk of human error and interference — a transposed number, a misread cheque, or worse. Second, there's no unified infrastructure underneath it. Every Major Giver maintains its own process, its own charity banking database, and its own verification methods. Most of those methods involve a scanned image of a void cheque.

Some larger platforms use intermediary payment processors. These tools handle the file creation and submission, but they typically charge a percentage of the transaction — a model we'll come back to later in this series, because it has significant implications for major giving.

Why this matters for major giving

Canada's charitable sector holds over $260 billion in assets. Donor Advised Funds are one of the fastest-growing vehicles for major giving, with consistent year-over-year growth. Foundations disburse billions annually. Corporate giving programs move significant capital into the sector every year.

The dollars are significant. The infrastructure moving them is not.

While the rest of the economy races toward real-time, data-rich, 24/7 payment rails, charitable disbursements are still batch-processed during business hours, manually verified against paper documents, and dependent on charity banking data that may be months or years out of date.

This isn't a technology problem in the traditional sense. The technology to do better exists — it's the same technology that lets you instantly verify a bank account when you sign up for a new fintech app. The problem is that nobody has built that technology into a system designed specifically for how Major Givers actually disburse to charities.

The gap between consumer payments and charitable payments

Here's the contrast that should bother anyone working in this sector:

You can send $3,000 to a friend via Interac e-Transfer in seconds. The account is verified. The funds are confirmed. You get a notification when it's done.

But sending a $50,000 grant from a Major Giver to a registered Canadian charity? That might take weeks. It involves email chains to collect banking data, manual entry into a batch file, and a void cheque that proves someone has a chequebook — but doesn't prove the account belongs to the charity it claims to represent.

A void cheque is not a verification method. It's a photocopy of a piece of paper. In 2026, that's what a significant portion of Canada's charitable infrastructure depends on.

What's ahead

The payment rails are modernizing. Payments Canada is expanding access. The Real-Time Rail is coming. New compliance standards from FINTRAC are tightening how EFT transactions are verified and documented.

The question is whether charitable disbursements will modernize with them — or continue to rely on infrastructure the rest of the economy has already outgrown.

In the next post, we'll look at what happens when that gap creates real consequences: the fraud, the friction, and the hidden cost of every organization in the sector building and maintaining its own DIY disbursement process.

WellFunded's Disbursement Hub is purpose-built EFT infrastructure for Canadian charitable disbursements — zero transaction fees, institutional-grade bank account verification, and shared charity banking data that benefits every funder on the network.

This is the first post in our series on charitable disbursement infrastructure in Canada. Read Part 2: The Real Cost of DIY Charitable Disbursements and Part 3: Shared Infrastructure for Charitable Disbursements.

Keep reading

The Real Cost of DIY Charitable Disbursements

Fraud, stale data, broken trust, and absurd fees — the hidden cost of every organization building its own disbursement process.

Shared Infrastructure for Charitable Disbursements

What charitable disbursement infrastructure should look like in 2026: verified, shared, zero-fee, and built for major giving.

The Verification Gap: Why DAF Disbursements Are Exposed

A void cheque proves an account exists, not that it belongs to the charity. Why charitable disbursement controls are failing, and what actually closes the gap.

Ready to modernize your philanthropy?

See how WellFunded can help your organization make better funding decisions.