Shared Infrastructure for Charitable Disbursements

What charitable disbursement infrastructure should look like in 2026: verified, shared, zero-fee, and built for major giving.

Jeff Golby

CEO & Co-Founder, WellFunded

Key Takeaways

- The solution isn't a better version of the old tools — it's shared infrastructure with structural safeguards

- One centralized, verified repository of charity banking data eliminates the DIY model and its risks

- Zero transaction fees make modern disbursement infrastructure viable for major giving for the first time

If you were designing charitable disbursement infrastructure from scratch — knowing everything we know about fraud risk, banking verification technology, and the needs of major giving — what would you build?

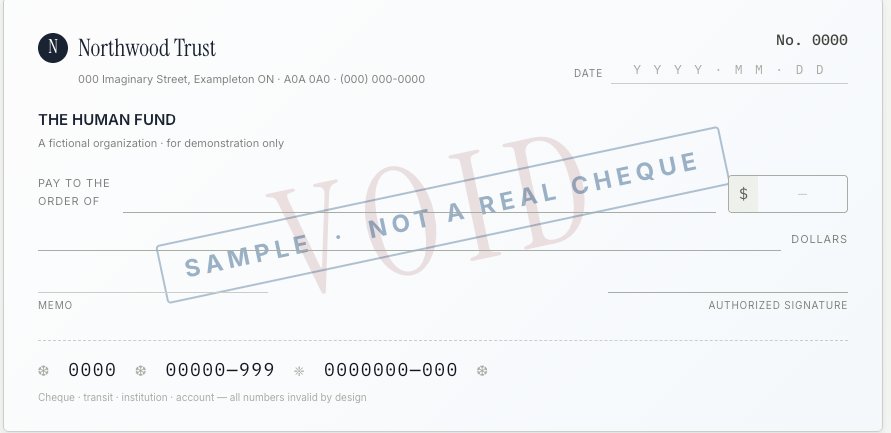

You wouldn't build another siloed tool. You wouldn't build another percentage-based platform. And you certainly wouldn't build something that depends on void cheques and emailed PDFs.

You'd build shared, secure infrastructure with guardrails. Not siloed, sloppy software held together by trust and spreadsheets.

Here's what that looks like.

One centralized, verified repository

Every charity's EFT data in one place. Verified through institutional-grade banking authentication — the same infrastructure used by Canada's major financial institutions. Not void cheques. Not emailed PDFs. Not a spreadsheet someone updates manually.

Account ownership verified, not just numbers collected. When a charity connects their bank account, the system confirms that the account belongs to the registered charity — through the same technology that verifies your bank account when you link it to a fintech app. The difference is that this verification is purpose-built for the charitable sector.

Charities update their banking data once. Every funder on the network benefits immediately. No more every-organization-maintaining-its-own-database. No more duplicated effort. No more stale data discovered only when a transfer fails.

This is the network effect that makes shared infrastructure fundamentally different from another software tool. Every charity that joins makes the system more valuable for every funder. Every update benefits everyone.

Humans out of the loop where it matters

The biggest fraud risks in charitable disbursements come from human access to banking data and fund flows. The previous post made this clear — when people can see the money or the routing numbers, the system depends entirely on individual integrity.

The right design minimizes human touchpoints. No one on the DAF side, the platform side, or the charity side should need to see raw banking numbers. Authorization and fund movement happen through secure, auditable infrastructure. The platform facilitates the connection — it never holds or touches the funds.

You can't steal what you can't see. You can't redirect what you don't control.

This isn't about assuming bad intent. It's about building systems that don't require good intent to function safely. That's what real security architecture looks like.

Built for frequency, not one-off interactions

We covered the frequency problem in the previous post: the individual DAF-to-charity relationship may be infrequent, but the collective relationship — across all DAFs, foundations, and corporate funders — is continuous.

Shared infrastructure turns infrequent individual touchpoints into a persistent, current data layer. A charity that receives one grant per year from a given DAF still has their banking data verified and up to date — because they're receiving grants from other funders on the same network. The system prompts them to keep their information current, and they have a direct incentive to do so: it's how they get paid.

No more stale data. No more first-sign-is-a-failed-transfer. No more DAF administrators making awkward phone calls to charities who don't know what a Donor Advised Fund is.

Here's the standard this should create: from the moment a fund holder, foundation, or corporation signals their intent to give, to the moment the charity receives the funds — that should take a week. Not a month. Not "whenever we get around to the next batch." A week. If a donor has made their decision and the grant is approved, there is no reason the charity should be waiting longer than that. Verified banking data, shared infrastructure, and automated processing make this possible. It should be the baseline expectation for every Major Giver in Canada.

No percentage fees

Zero transaction fees. Period.

A $100,000 grant costs the same to process as a $100 one. The platform never touches the money — it facilitates authorization and connection only.

This is the structural change that makes modern disbursement infrastructure viable for major giving for the first time. The reason DAFs and foundations haven't widely adopted digital disbursement tools isn't that they don't want to modernize. It's that a percentage-based fee model becomes absurd at scale. A foundation disbursing tens of millions of dollars a year shouldn't be paying hundreds of thousands in transaction fees for what amounts to a verified bank transfer.

The technology to verify accounts and reduce risk has caught up. The pricing model should reflect that.

Flexible enough for real workflows

Infrastructure that works in theory but doesn't fit how organizations actually operate isn't infrastructure — it's a demo.

The right system handles the core functions well and stays flexible where it matters. That means custom development to match client workflows, not forcing every organization into the same rigid process. It means automatically generating the authorization documents organizations need — like board minutes to approve a disbursement batch. It means working for DAFs, foundations, and corporate funders, each of which has different compliance requirements and internal processes.

KYC compliance built in. Complete audit trails for every transaction. Real-time status visibility from approval to deposit. The core done well, with the flexibility to accommodate the edge cases that every organization has.

Built by Canadians, for this moment

Canada's banking infrastructure is in the middle of its biggest modernization in decades. The Canadian Payments Act just expanded who can access national payment systems. The Real-Time Rail is coming. New compliance standards from FINTRAC are tightening how EFT transactions are verified and documented.

The charitable sector should be modernizing alongside these changes — not lagging behind them.

WellFunded's Disbursement Hub is purpose-built for this moment. Connected to institutional banking infrastructure through a technology partner trusted by 300+ Canadian financial institutions. Designed specifically for how charitable disbursements actually work in Canada — the batch processing, the compliance requirements, the need for charity-validated data.

This is Canadian infrastructure for Canadian philanthropy. Not a payment tool adapted from another market. Not a generic fintech product with a charity label on it.

The shift

The philanthropic sector doesn't need a slightly better version of what it has. It needs shared infrastructure built for how major giving actually works — secure, verified, zero-fee, and designed so that every dollar reaches the charity it was intended for.

That's what we built.

Book a demo to see how Disbursement Hub works for your organization.

This is the third post in our series on charitable disbursement infrastructure in Canada. Read Part 1: How Charitable Dollars Actually Reach Charities and Part 2: The Real Cost of DIY Charitable Disbursements.

Keep reading

The Real Cost of DIY Charitable Disbursements

Fraud, stale data, broken trust, and absurd fees — the hidden cost of every organization building its own disbursement process.

How Charitable Dollars Actually Reach Charities

Canada's payment infrastructure moves $411B daily. Charitable disbursements still rely on void cheques and manual batch files.

The Verification Gap: Why DAF Disbursements Are Exposed

A void cheque proves an account exists, not that it belongs to the charity. Why charitable disbursement controls are failing, and what actually closes the gap.

Ready to modernize your philanthropy?

See how WellFunded can help your organization make better funding decisions.